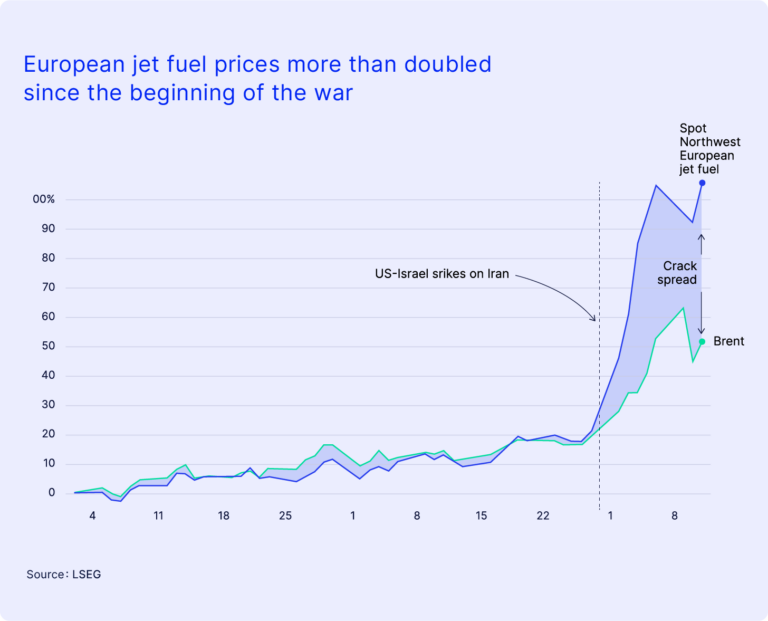

As tensions in the Middle East escalated, jet fuel prices spiked, more than doubling since the start of the year. Bunker fuel prices in ocean freight also rose by over 70% month-on-month.

These sharp increases highlight how quickly geopolitical developments can impact energy markets and expose global logistics to broader risks.

For supply chains, such volatility has become a recurring feature in recent years. For logistics teams, it means rising expenses, greater operational complexity, and reduced predictability in pricing and planning.

In this article, we examine the operational impact of fuel dependency and ongoing volatility, and how the industry is beginning to respond to these pressures.

What’s driving fuel price volatility

Fossil fuels are the primary energy source for global logistics across both air and ocean freight. As a core cost driver, they can leave companies directly exposed to external shocks.

The fuel market is characterized by uneven supply distribution and limited jet fuel refining capacity, while continued reliance on fossil fuels leaves few short-term alternatives when conditions change.

Together, these conditions make the market especially sensitive to disruption and prone to rapid price fluctuations. This volatility is a major factor impacting logistics planning globally.

Operational impact

Fuel price volatility is amplifying pressure on supply chains and affecting the day-to-day work of logistics teams.

Across transport modes, carriers are adjusting operations to manage disruption and rising costs.

Airlines are adjusting rotations, capacity and routes to maintain service continuity, reducing flexibility and adding to less predictable transit times. At the same time, higher fuel prices are increasing operating expenses and driving the use of surcharges.

In turn, this leads to increased transport rates, while reduced cost visibility makes budget forecasting more complex for logistics companies.

In ocean freight, the suspension of key routes such as the Strait of Hormuz and the Suez Canal has forced carriers to cancel sailings or divert vessels, raising fuel consumption and amplifying cost and schedule variability across trade lanes.

Taken together, these factors are directly impacting how logistics teams plan and manage shipments. Many are now favoring modal shifts (including rail and road) and alternative routes to control spend and maintain reliability.

Overall, companies are facing reduced operational flexibility, greater variability in lead times and continued pressure on costs and margins.

“We’re seeing customers place much greater emphasis on cost visibility and planning flexibility. In air freight, this is driving more cautious booking behavior and a preference for options that allow changes when needed. In many cases, customers are willing to accept longer transit times, but are far less willing to absorb additional cost increases.”

Christopher Braun

Director Air Freight, Forto

Why volatility keeps recurring

Fuel price volatility is not a one-off event in logistics, but part of a recurring pattern.

Supply is unevenly distributed across regions, and refining capacity, particularly for jet fuel, is constrained.

Even short-term disruptions can tighten availability and drive rapid price fluctuations.

At the same time, the energy system underpinning global logistics is relatively slow and inflexible, built around fixed infrastructure and established supply routes, which hinder how quickly operations can adjust when conditions change.

Because these structural constraints limit the system’s ability to absorb shocks, disruptions are not easily smoothed out and instead repeatedly trigger price volatility.

Geopolitical factors further amplify these dynamics. For example, recent restrictions on refined fuel exports by China removed critical supply from the market, reducing availability and driving price fluctuations across entire regions.

Against this backdrop, the transport industry’s continued reliance on fossil fuels, with few short-term alternatives for both air and ocean freight, increases its exposure to recurring volatility.

As a consequence, companies are facing increasing pressure to manage its impact on operations.

In parallel, regulatory requirements are adding further momentum to a broader shift away from fossil fuels, reinforcing the need for longer-term structural change.

A shift toward energy diversification

Market dynamics, regulatory mandates (e.g. ReFuelEU aviation & FuelEU Maritime), customer expectations, and corporate sustainability targets are shaping how companies approach fuel use. Longer-term considerations around cost, energy availability and supply security are further reinforcing this.

Adoption of sustainable fuels

The use of sustainable fuels, including biofuels, is gradually gaining traction across both air and ocean freight. In air freight, Sustainable Aviation Fuel (SAF) is a key focus area, although availability remains limited. SAF currently accounts for less than 1% of global jet fuel supply, underscoring the challenge of scaling production. High production costs, constrained feedstock availability, and infrastructure limitations continue to hinder adoption, even as demand grows.

Electrification

Electrification is expanding across certain transport segments, particularly in short-haul and regional operations, as electric vehicle production and battery capacity continue to scale. China alone accounts for more than 60% of global EV output and around 80% of battery manufacturing.

However, its application in air and ocean freight is still constrained, and translating this into widespread adoption across logistics networks remains complex due to infrastructure requirements and high energy demands.

Investment in alternative energy

This trend is also reflected in the scale of capital flowing into alternative energy and related technologies. Global clean energy investment now exceeds $2 trillion annually, roughly double that of fossil fuels, highlighting the level of commitment behind the transition.

However, as a recent McKinsey report highlights, progress remains uneven and much of the required infrastructure and technology is still in early stages of deployment.

How Forto supports the transition

While fuel surcharges remain a core part of today’s operational reality, companies need to manage cost volatility alongside the shift in energy sources. At Forto, we provide the tools and expertise to help customers navigate this dual challenge.

Managing volatility

- Detailed insights into cost drivers help teams understand how fuel impacts shipments.

- Planning and forecasting tools help anticipate cost fluctuations.

- One-to-one support enables faster, more informed decision-making in a volatile environment.

Enabling the transition

- Our sustainable fuel solutions, including SAF and biofuels, allow customers to begin reducing emissions without disrupting existing supply chains.

- Flexible models enable gradual adoption, aligned with both operational needs and regulatory requirements.

Together, these capabilities help guide teams through this period, as they balance immediate cost pressures with longer-term structural changes.

Adapting to a changing energy landscape

Fuel price volatility will remain a defining factor in global logistics. At the same time, it is reinforcing a broader move toward more diversified and resilient energy sources.

For supply chain teams, the challenge is not only to manage ongoing disruption, but also prepare for a structural transition.

Companies that can respond to both will be better positioned to maintain stability today while building more resilient supply chains for the future.

If you are looking for a strong partner that supports you in navigating ongoing volatility and preparing for this transition, get in touch with our team.