Operational update

Middle East

This page is updated as new information becomes available. The rolling update log at the bottom contains the most recent entries.

Operational update

This page is updated as new information becomes available. The rolling update log at the bottom contains the most recent entries.

Following the military escalation between the US, Israel, and Iran on 28 February–1 March 2026, transport operations across the Middle East have been significantly disrupted. The situation remains dynamic. This page will be updated as new information becomes available.

Your Forto contact will reach out directly if your specific shipment is affected.

For immediate queries, contact us here:

https://forto.com/en/contact-us

The late-June reopening has stalled and reversed. The US–Iran ceasefire has broken down: after attacks on commercial vessels in the Strait early in the week, the US struck Iranian coastal and port targets over 7–9 July, and Iran retaliated with missiles and drones against US bases in Kuwait, Bahrain, Qatar and Jordan. The US has stated the interim agreement is “over.”

Transit has collapsed again – no AIS-visible large-vessel crossings on the US-coordinated Omani-coast route since 7 July. The IMO evacuation scheme remains suspended since 25 June, with ~11,000 seafarers still stranded. Carriers have not resumed scheduled Gulf services, and Cape of Good Hope routing stays the baseline for Asia–Europe.

Last updated: 22 July 2026, 9:45

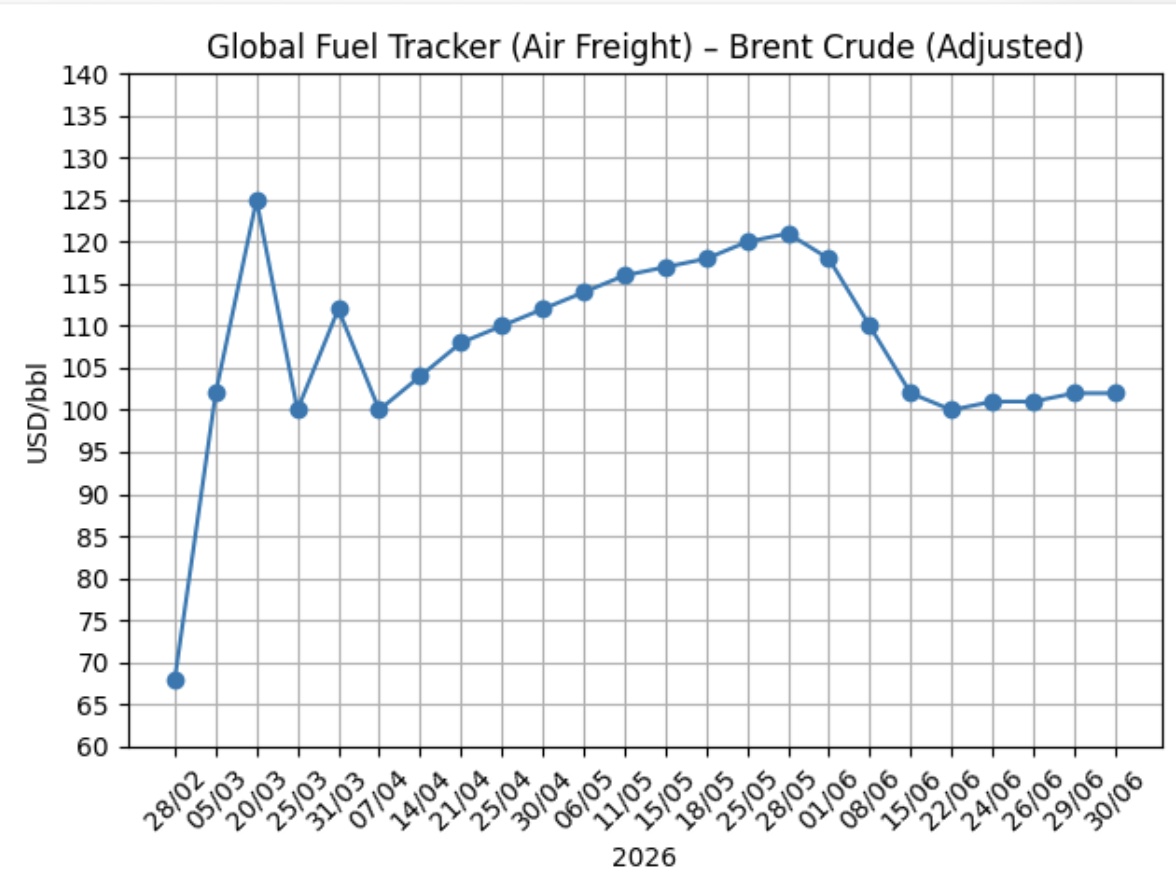

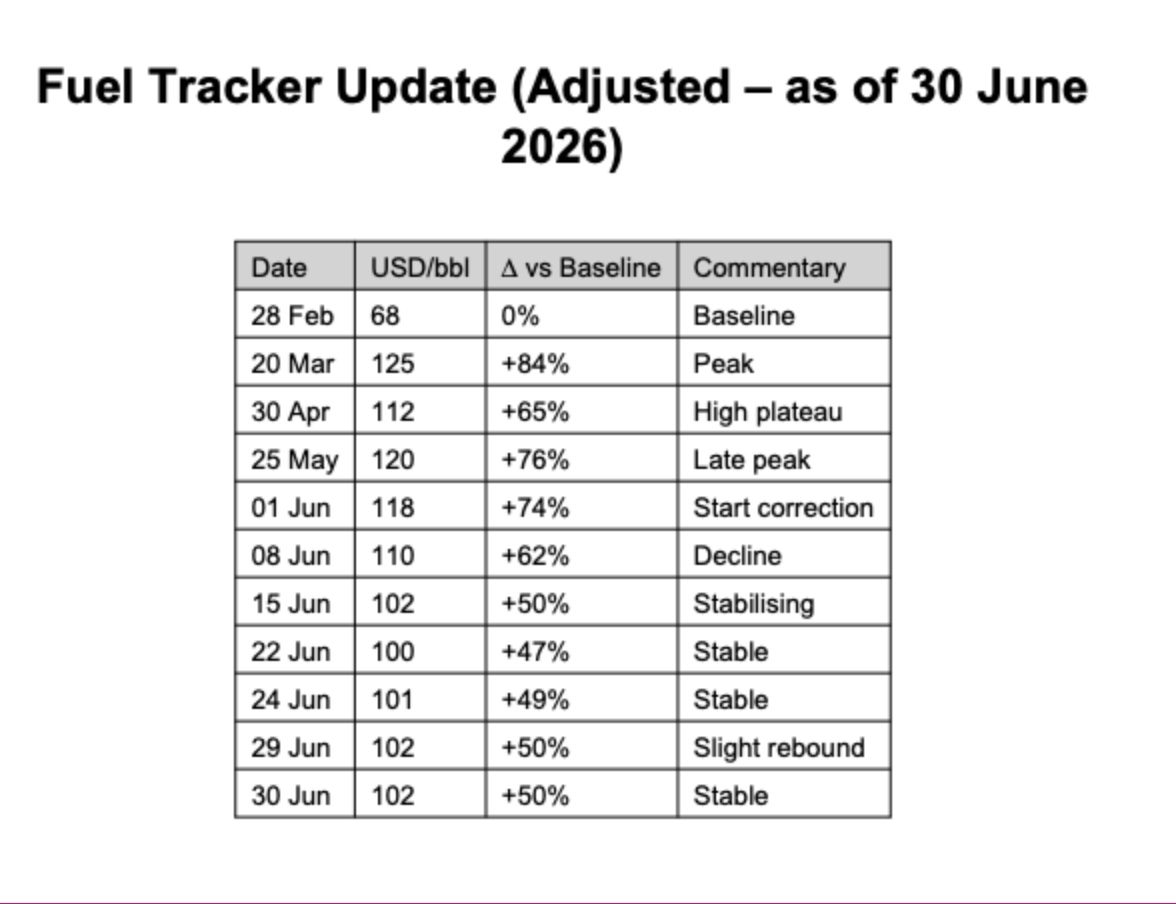

Last updated: 30 June 2026, 13:00